Credit & Debit Card

Processing

Accept payments anywhere, anytime...

What is Credit Card Processing?

The safe handling and authorization of electronic payments made with credit or debit cards is known as credit card processing. It entails sending card information, confirming the identification of the cardholder, and transferring money from the cardholder's account to the merchant's account. Card swipes or data entry, authorization requests, approvals, settlement, clearing and funding, statement production, and payment are just a few of the phases that are involved in the process. Businesses can accept card payments through credit card processing, which involves a number of parties including the merchant, cardholder, card networks, issuing bank, and payment processor. This mode of payment is safe and effective.

10 Advantages of Utilizing AuthoPay for Your Credit Card Processing

Making the choice to include credit card processing in your company's operations is a major step that opens up a world of possibilities. You can now reach a worldwide audience as a small business owner by expanding your customer base past your own neighborhood. Discover the following factors that are motivating an increasing number of business owners to choose AuthoPay:

Streamlined Digital Payments

Trackable Transactions in the Digital Realm

Enhanced Protection Against Chargebacks and Fraud

Complete PCI Compliance

Flexibility to Accept Card Payments Anywhere

Offering Convenient Payment Options

Securely Encrypted Transactions for Added Security

Easy and Convenient Contactless Payments

Expanding Reach to a Global Customer Base

Building Customer Confidence and Trust

How Does Credit Card Processing work?

Card swipe or data entry, authorization request, approval, settlement, clearing and financing, statement creation, and payment are the many procedures involved in credit card processing. When a customer makes a transaction, the issuing bank or payment processor receives their card details for authorization. Once a transaction has been approved, the specifics are included to a batch that is later settled with the cardholder's bank. The merchant receives money from the transactions after deducting processing fees, and the cardholder receives a billing statement and pays their bank. Through this cooperative procedure, businesses are able to accept credit card payments from clients in a secure and effective manner.

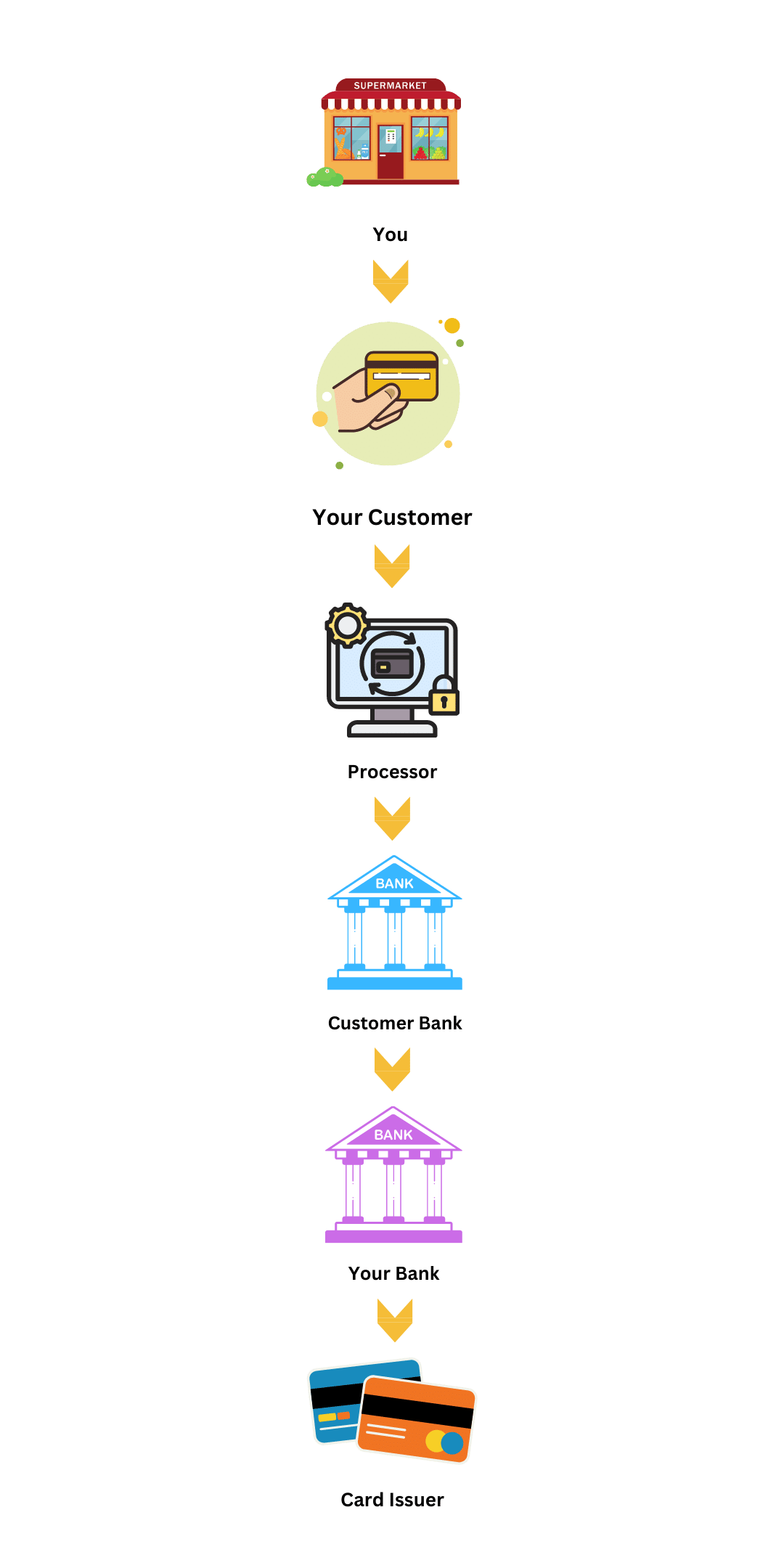

The 6 Entities Needed To Process A Transaction

While the act of processing a credit card occurs within seconds, multiple entities participate in the overall process.

Your Business (Merchant). Your company, acting as the merchant providing goods or services in exchange for consumer payments, is the main player in the credit card processing.

Your Customer (The Cardholder). Your consumer, who has a credit or debit card they want to use for the purchase, is an additional party involved in credit card processing. The client assumes the position of "cardholder" in this scenario.

Your Credit Card Processor (Payment Processor). Is the organization in charge of facilitating the exchange of transaction data between your company and your client. They function as your contractual mediator, working with you to agree on conditions and processing costs.

Your Customer’s Bank (The Card Issuer). The credit or debit card possessed by your customer is coupled with a bank account, which can be a major financial institution like Wells Fargo or Bank of America, or a smaller business such as a credit union. The bank responsible for holding the account and issuing the credit or debit card to your customer is referred to as the "card issuer.

Your Bank (The Acquirer). Your acquiring bank is the financial institution where you keep your company account and that gives you the ability to accept credit card payments.

Your Customer’s Card’s Brand (The Network/Association). The network or organization that runs and oversees the payment system is represented by the payment card brand connected to your customer's card, also known as the card network or card association.

7 Steps To Processing Credit Card Transactions For Small Business

Step 1: Transaction Initiation by the Customer

In order to complete a transaction at the merchant's establishment, the cardholder (consumer) swipes, taps, or inserts their card to start the credit card payment procedure.

Step 2: Information Acceptance by the Merchant

The merchant then securely obtains and gathers the cardholder's payment information via telephone, internet platforms, or in-person contacts.

Step 3: Transmission of Information

The merchant then proceeds to manually or automatically transmit the funds to the payment processor through a variety of channels, such as online using a payment gateway or by keying the information into a virtual terminal.

Step 4: Verification of Information

The issuer, or cardholder's bank, receives the transactional information from the network. The issuer then double-checks its records to confirm the authenticity of the information supplied and confirms that the cardholder has enough money on hand to complete the transaction. To ensure a secure transaction procedure, the processor simultaneously undertakes fraud detection techniques and runs a data security scan.

Step 5: Notification to the Processor

The issuer notifies the processor with a "approved" or "declined" message following verification, depending on the supplied information. This procedure takes a little time. The transaction is only partially complete because the merchant has not yet received payment, even if an approval enables the client to make the purchase. On their bank statement, the customer notices an authorization or pending charge that temporarily reserves the funds.

Step 6: Closure of the Transaction Batch

The merchant must start the batch's closure in order to transfer money from the customer's bank account to their account. A batch is a group of transactions. The batch can be shut down manually, allowing for any number of desired transactions, or programmed to shut down automatically after a specified amount of time. Batches are often closed in cycles of 24 hours, which is the custom.

Step 7: Funds Transfer

Once the batch has been properly closed, the merchant notifies the processor that all of the transactions in it are accurate, complete, and valid. The processor then permits the transfer of money between the merchant's account (acquiring bank) and the customer's bank account (issuing bank) across the network. The transaction is now regarded as finished.

How Do Fees Work For Payment Processing?

Let's discuss fees now that you are familiar with the parties involved and the procedures in credit card processing. While we will go over some typical fees in this article, you may refer to our extensive guide on credit card processing fees for a thorough breakdown.

Service Fees

Your processor's monthly bill comprises the following key categories:

Transaction Fees

These fees make up the majority of your overall costs and are connected to specific transactions. They include interchange and retail fees as well as set percentage or flat rate costs applied to transactions. Examples include fixed % markup rates or permission fees.

Recurring Fees

These charges are unrelated to specific transactions. They include monthly fees for services like account on file, statement, batch, and PCI compliance, non-compliance, and compliance.

One-time Fees

Setup costs, early termination fees, chargeback or retrieval fees are examples of one-time fees that happen on particular or unique circumstances.

Pricing Models

Each month, payment processors use different pricing strategies to collect fees, which has an impact on your company's prices (ranging between 2 and 4 percent on average). The pricing model and overall cost are influenced by things including your business strategy, the industry risk level, how you accept credit cards, and more.

Interchange Plus / Percentage Markup: This clear but complicated price structure includes wholesale expenses that are charged to you, such as association fees and interchange rates. To pay the payment processor, a modest fixed percentage markup is added to the cost.

Flat Rate: With this streamlined price structure, each month's rates and fees are combined into a single, straightforward flat percentage. It is frequently utilized by PayPal, Square, and Stripe.

Tiered/(E)RR: Similar to flat rate pricing, the tiered structure divides transactions into three categories based on interchange rates: qualified, mid-qualified, and non-qualified. Accordingly, your processor will charge you.

Surcharge: The transaction fees are passed down to your clients through this price structure. Only transactions that might result in processing fees are covered by it. In contrast to cash discounts, surcharge programs pass the expense on to the customer, which lowers your processing costs.

Different Credit Card Processing Terminals

Exploring Your Equipment Options for Credit Card Transactions

The choice of equipment is important when it comes to processing credit card transactions. You establish a connection with your payment processor using credit card readers created expressly for this use. However, a number of factors will determine the best equipment for you:

Payment Processor Support: Consider the compatibility with your chosen payment processor.

Business Needs: Evaluate whether you operate in-person or online, require mobility, or need additional features like inventory management.

Cost and Long-term Viability: Assess the solution's affordability and future scalability.

POS Systems:

In addition to handling credit card processing, POS systems—which are often used in retail and restaurant settings—also provide extra capabilities like inventory management and seamless interaction across various parts of your business.

Virtual Terminals:

Through a secure interface, you can accept credit card transactions thanks to these online software solutions. Because they permit manual entry of card information, virtual terminals are perfect for firms that conduct mail or telephone orders.

Payment Gateway:

Payment gateways serve as middlemen between your online store and the payment processor, securely transmitting transaction data, verifying payments, and ensuring industry compliance.

Mobile/Wireless Terminals:

Mobile and wireless terminals are becoming more and more common in retail settings because they offer flexibility and portability. While wireless terminals function cordlessly and connect to the internet via WiFi or cellular networks, mobile terminals use smartphone apps to execute transactions.

EMV Terminals:

In order to provide greater security, EMV technology replaces conventional magnetic stripe cards with chip-enabled cards. The integrated chip is read by EMV terminals to safely process payments.

Online Shopping Carts:

Online shopping carts, which are crucial for e-commerce companies, incorporate a virtual terminal on the backend, enabling users to autonomously make purchases through a user-friendly online store.

By considering these options and assessing your specific requirements, you can choose the most suitable credit card processing terminal for your business.

Unlock seamless credit card processing today for smooth transactions.

Selecting the Right Credit Card Processor: A Guide

You ought to know how to take credit card payments for your company by this point. Let's now explore how to choose the ideal credit card processor for your unique requirements. Making a pick from among the many credit card processing firms is crucial since it can have a significant effect on how quickly your business expands.

Cost is a critical element, but it's also necessary to take other features of a credit card processing firm into account. Consider elements like the accessibility of customer service, equipment compatibility with your needs as a business, and, most crucially, the security of your business transactions.

Merchant Services

Your merchant services provider, who offers a variety of financial services specifically designed for businesses, is your credit card processor. Credit card processing is the most frequent service provided. The features of merchant services may also include ACH (automatic clearing house) transactions, electronic checks, processing for physical checks, gift card programs, loyalty programs, and more, depending on the nature of your business.

Additional Services

In addition to the core merchant services, credit card processors may offer a variety of supplementary services, including:

Merchant cash advances or loans

Payroll management

Inventory management

Accounting and invoicing services

Customer loyalty programs

Fraud prevention tools

Integrations

You will have access to complete solutions thanks to the integrations that many payment processors offer with other service providers. Examine their integration options if there is a specific service you need that your credit card processor does not provide.

PCI Compliance

The PCI Security Standards Council created the stringent security requirements known as PCI Compliance (Payment Card Industry Data Security Standard). For the credit card processing industry to experience less fraud and related costs, compliance with these standards is essential. It's crucial to pick a credit card processor who complies with these requirements and is ready to help you achieve and maintain your own compliance.

Fraud and Risk Protection

Accepting credit cards involves some dangers, such as the possibility of chargebacks and fraudulent transactions. By exercising due diligence, these risks must be reduced. Customers are protected from fraud and have the option to challenge transactions, which might result in chargebacks. Your company's operations and sector affect the likelihood of chargebacks and fraud. A trustworthy merchant service provider will put your needs first and work to reduce your risk of fraud and chargebacks, which will ultimately save you time and money.

In conclusion, choosing the best credit card processor requires taking into account aspects other than price. Finding a provider who provides complete merchant services, other pertinent services, integrations, PCI compliance, and strong fraud and risk prevention is necessary. By taking the time to select the ideal credit card processor, you can minimize any risks while ensuring secure and convenient transactions for your company.

Our payment gateways, which are fully compliant with PCI standards, offer automated protection against fraud and help reduce the occurrence of chargebacks. These gateways can seamlessly integrate with various systems, including:

CVV requirements

Velocity settings

Specified ticket parameters

IP velocity settings

Limited access to specific geographical locations

Chargeback detection

Analytics that identify vulnerabilities

FAQ'S

What types of credit cards does AuthoPay's Credit Card Processing support?

AuthoPay's Credit Card Processing supports all major credit card brands, including Visa, Mastercard, American Express, Discover, and more. This ensures that businesses can cater to a wide range of customers with different credit card preferences.

Is AuthoPay's Credit Card Processing secure for processing sensitive card data?

Security is a top priority at AuthoPay. Our Credit Card Processing service utilizes advanced encryption and complies with industry security standards, ensuring that all card data is securely handled during the payment process. Customers can trust that their information is safe and protected.

I've recently launched my business. How do I get started with accepting credit card payments?

Explore credit card processing for small businesses with AuthoPay. Get a free account for online and in-person payments, retail POS with AuthoPay Card Reader, or create an online store. Use online invoicing and set up subscription plans. Simplify payments with AuthoPay! Choose AuthoPay for seamless payment solutions tailored to your business needs.

How quickly are funds settled into my account with AuthoPay's Credit Card Processing?

AuthoPay ensures timely settlement of funds to merchants. Typically, credit card transaction funds are deposited into your designated account within 1-2 business days, helping you maintain a healthy cash flow for your business.

Already working with another credit card processing company?

No worries! Transitioning to AuthoPay is hassle-free. If you have questions about switching, leaving a contract, or anything related to the industry, our Merchant Experience team is here to assist with guidance and honest advice. We're dedicated to making your switch to AuthoPay a seamless experience.

Can I process credit card payments online and in-person with AuthoPay's Credit Card Processing?

Yes, AuthoPay's Credit Card Processing is a versatile solution that caters to both online and in-person payment processing. Businesses can accept credit card payments through their website or use AuthoPay's card reader to process payments at a physical point of sale.

Start Today with AuthoPay

If you're looking for an affordable, dependable, and well-supported payment platform, AuthoPay's merchant accounts are the ideal solution for your business. Get started now and experience the benefits firsthand.

US Head Office

111 North Orange Avenue, Suite 800, Orlando, Florida, 32801

Contact

© 2024 AuthoPay.Ai - All Rights Reserved

Industries Serviced

Accepting Payments